Introduction

More than halfway into 2020, Pembroke’s physical offices remain closed due to the pandemic and our team continues to operate at full force from home. Under these circumstances we have increased our internal communications with firm wide “town hall” meetings and functional team meetings and embraced a shared commitment to “survive and thrive”. We have also enjoyed intensified communications with our clients and have an exciting agenda of virtual manager lunches, written communications, and workshops planned for the second half of 2020.

We hope that you will find this reformatted version of our Pembroke Perspectives Newsletter to be both interesting and informative and we would welcome the opportunity to speak with you should you have any questions or comments.

On the Road Conference – COVID-19 Realization and Response

The Pandemic as Accelerant

Our On the Road series takes a wide-angle view this quarter looking at the bigger picture

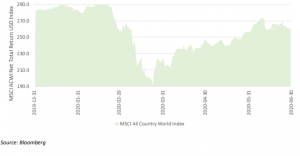

It is the nature of crashes that they occur suddenly. Looking back on the first half of 2020, it is nevertheless, hard to find historical precedent either for what has taken place in the global economy and world stock and bond markets, or how quickly it has transpired. The MSCI All Country world Index (ACWI), one of the broadest indices of global stocks, gives a sense of the scale and proportion of events. At the end of 2019, the index had a market capitalisation of a little over USD 50 trillion, equivalent to about 57% of 2019 global GDP of USD 88 trillion.1

From February 17th to March 20th, the index declined 34%, a loss in value on the order of USD 17 trillion in 25 trading days. By the end of the second quarter, the index had returned to within 6% of its beginning-of-year level (Exhibit 1).

Exhibit 1: MSCI All Country World Index Performance During First half of 2020

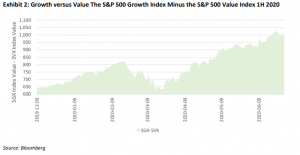

The remarkable recovery in the ACWI’s market value, however, belies tectonic share-shifts that have taken place within it. Technology, whether it is under the hood of our cars, supporting our virtual meetings and conferences, or managing the supply chains of e-commerce, is disrupting incumbent businesses at an accelerating pace. The ACWI information technology sub-index gained 14% in the first half of 2020. By contrast, the ACWI energy sub-index lost 34%. There are indications that this is but one of the many systemic changes underway. Toward the end of the quarter, one of the world’s largest integrated oil and gas companies BP p.l.c., shared their view that the aftermath of the pandemic could “accelerate the pace of transition to a lower carbon economy and energy system…”2. At the core of that new system the company that wants to “Power Everything”, Tesla, gained over 150% in the first half of 2020. Its market capitalisation is now nearly as large as BP p.l.c. and Exxon Mobil combined. The notion of the pandemic as an accelerant of existing secular trends was a recurring theme in Pembroke’s 2020 virtual manager luncheon series and was by no means limited to energy or technology as our portfolio managers reviewed the prospects for market share gains by innovative disruptors in online shopping, telemedicine and telehealth, and digital financial services. On the losing side of these share-shifts, though, there has been a heavy toll. Already impaired, numerous once-dominant business models in traditional consumer retail, healthcare, transportation, energy, and industrial businesses suffered permanent impairment or became distressed during the period. The violent changes in these sectors reflect a quickening and convergence of secular technological, social, and environmental trends that are rupturing established models and systems and creating market-share shifts in favor of innovative disruptors. Capital is flowing to entrepreneurs who are both in tune to society’s demands and who are successful at managing growth. One perspective on these shifting capital flows is the widening performance gap between growth and value companies While the S&P500 Value Index (SVX) lost 12% in the first half of 2020, the S&P 500 growth index (SGX)

gained 12%.

One explanation for the scale and speed of capital redirection may be that market participants are increasingly recognizing the pandemic not as an event but as a wake-up-call. Covid-19 is but the latest in a series of emerging diseases including SARS, pandemic influenza H1N1, Avian Influenza, West Nile Virus, and MERS that may have been exacerbated by climate change. In May, The World Bank published Fighting Infectious Diseases: The Connection to Climate Change3 discussing the impact of changing weather patterns, air pollution, melting ice and permafrost, and global warming on infectious diseases. After months of global quarantine, travel restriction, and enforced distancing, the true sustainability of business models has been brutally tested. If it is realistic to envisage continued climate change, more frequent regional and global disease outbreaks, and more frequent natural disasters, it is realistic to envisage the continued outperformance of disruptive business models that respond to these exigencies and indeed go some way to reversing the trends behind them. Pembroke has always invested in innovation because innovation is a truly renewable resource. Companies that are relentlessly driven by new ideas are companies that can grow, respond to changing circumstances, or create their own new circumstances. In this way, innovation is at the heart of sustainability. The pandemic has demonstrated tangibly the fragility of myriad models (global food and medical supply chains, just-in-time inventories, testing and monitoring protocols, packaging and delivery systems, and fuel storage and supply systems, to name but a few). It has also shown how quickly governments, businesses, and consumers will migrate en masse to innovative alternative solutions. One of the reasons it has always been so important for Pembroke analysts and portfolio managers to go ‘on the road’ is to meet the new innovators and feel the excitement inside idea-driven organizations. While there is no substitute for this type of close-up company due diligence, there are moments as well when it’s important to recognize the wider-angle tipping points in the economy. As the summer of 2020 rolls on, it is becoming clearer that the economic toll of this pandemic is not going to be temporary. The pandemic is instead hastening and deepening secular changes that were already underway; societal

changes to the way we work, travel, consume entertainment, exercise, shop, and eat. The share shifts that have taken place in the first six months of 2020 may be only a harbinger of the new wave ahead.

Investment Commentary & Outlook

After one of the worst quarters on record for North American stocks, prices reversed sharply in the second quarter of 2020 as investors grappled with the implications of COVID-19 offset by aggressive fiscal and monetary stimulus and hopes for a vaccine. Locked down for weeks, economies from China to Europe to to Canada have started to re-open, giving further reason for optimism. At the same time, the medium-term and long-term effects of the virus on the global economy are unknown as it has caused massive dislocations and changes in industries from travel to retail to technology.

Against the backdrop of fear and skepticism, stocks confounded many investors with their rapid rise over the last three months. Pembroke is not a macroeconomic research firm, but believes that some possible drivers of the market’s gains include:

1. Fiscal stimulus: short-term measures enacted by governments around the world have helped many businesses maintain payrolls during the shutdown, and ordinary citizens have benefited from income and stimulus programs to keep money in their pockets.

2. Monetary stimulus: against a backdrop of falling employment and economic uncertainty, central banks have flooded their economies with cash. Why? First, to prevent a credit squeeze. Second, to guard against deflation. And third, to inflate assets prices – from home prices to stocks – so that already suffering consumers would not see the value of their homes and retirement plans collapse, which would have exacerbated the crisis. Essentially, central banks are forcing investors into “risk” assets to help drive economic growth by lowering the yield on less risky investments such as government bonds.

3. The market looks forward: while the COVID-19 crisis is real and ongoing, the market looks forward. Investors are betting that like many crises of the past, from wars to disease to depressions, this too shall pass.

4. Businesses have adapted: the use of technology has facilitated an incredible transformation of many businesses in a shockingly brief period. Retailers have moved more online. Group meetings have been replaced by video conferences. Companies have assessed and implemented cloud software to meet the changing ways they interact with their customers. Despite all the headwinds, the world economy did not grind to a lasting halt. Rather, some of best and most well-positioned companies have taken advantage of the circumstances to accelerate adoption of their products and services.

Will there be losers in all of this? Of course. Will some of the outcomes be extremely unfair and unforecastable? Certainly. But there will also be winners. It is the harshness and beauty of capitalism played out over an unusually brief period of time. COVID-19 has acted as an accelerant, fuelling shifts in business and consumer habits that were underway but taking a long time to develop. Work-from-home technologies, telemedicine, and e-commerce have all seen their fortunes jump with unforeseen speed. At the same time, other industries such as commercial real estate and travel are facing structural risks to demand. While Pembroke’s investment team expects the global economy to recover, “normal” might look very different than expected only six months ago. It is with that reality in mind that the firm’s portfolio managers and analysts are assessing current and prospective holdings.

What is Pembroke Doing in this Environment?

In the last issue of Perspectives and during our series of virtual lunches (available at www.pml.ca), Pembroke detailed its focus on balance sheets and its decision to reduce holdings facing structural

headwinds brought on by the virus. Many fast-growing companies with strong secular tailwinds will weather this crisis, with offerings so compelling that they can grow rapidly right through the disruption. Other more cyclical growth companies might see deferrals of purchases, but the likelihood that they encounter structural, longer-term headwinds is low. These include some healthcare businesses, such as Pembroke holding Globus Medical (“GMED”), which sells equipment used in back surgeries. Conversely, some companies have seen their end markets dramatically altered. These include movie theatres and travel businesses. The investment team is spending a lot of time understanding which of its companies should continue to grow or at least see a full recovery in demand for their services, and which might be at risk of a lower demand environment for the foreseeable future. As long as the current period of significant uncertainty exists, balance sheet strength will remain paramount.

The investment team believes that the combination of muted global GDP growth and low interest rates should continue to favour growth stocks, but that careful stock selection is critical given the challenges and opportunities facing many companies. While we remain optimistic that the COVID-19 crisis will pass, its effects are likely to be long-lasting. Each company’s shifting competitive landscape and growth prospects need to be carefully weighed against valuation considerations. The siren song of fast-growing companies in areas such as software-as-a-service, trading at increasingly inflated prices, poses a real risk. These companies offer products and services compelling enough that they are able to continue their rapid growth despite the economic disruption caused by COVID-19. Pembroke has holdings in some of these exciting companies, but the investment team manages its portfolio weightings based on their competitive advantages, the sustainability of their growth rates, and their balance sheets. At the same time, we remain committed to running diversified portfolios, continuing to hold positions in companies with strong track records but which fall outside the “hot” areas of the market. The firm’s 52-years of experience indicate that market trends can change quickly, and that stock selection should be based on fundamentals rather than market momentum. Overall, the investment team is taking a balanced approach to its focus on growth stocks, with portfolios made up of high-growth businesses combined with more modest growers that are profitable, well-financed, and positioned to win market share over time.

Outlook

While the ongoing Pandemic creates significant uncertainty, Pembroke maintains a healthy outlook for North American small and mid-capitalization growth equities despite the headwinds posed by COVID-19. Many companies in both the Canadian and US portfolios should grow through this crisis, and those that have faced more serious disruptions are financed to survive and eventually thrive. The investment team has been impressed by how quickly many holdings have adapted, with retailers such as Aritzia re-focusing their efforts on e-commerce and leisure companies such as LCI Industries and BRP ramping up production to meet rising demand. Further, important trends in technology, such as software’s migration to the cloud, and in healthcare, such as home-based care, are accelerating.

The lingering policy effects of the financial crisis of 2008/2009, stresses in global trade, demographic pressures, and COVID-19 are contributing to lower global GDP growth and to keeping interest rates low. The firm remains committed to running portfolios diversified across industry sectors and to investing in companies that are well-positioned to deliver revenue and earnings growth over a multi-year period. In short, the firm’s approach to growth stock investing remains unchanged.

Canadian Equity Strategies

CANADIAN GROWTH EQUITY STRATEGY – Q2 PORTFOLIO COMMENTARY

Pembroke’s Canadian equity portfolios experienced a strong rally in the second quarter of 2020, rebounding from an extremely challenging start to the year. While the COVID-19 pandemic remains incredibly disruptive to lives and businesses on a global scale, actions taken by monetary and fiscal authorities to counter the economic fallout from containment measures appear to have comforted investors. Significant uncertainty remains as to the ultimate severity and duration of the outbreak, but market participants are looking through near-term disruptions.

While strong absolute equity market returns in the second quarter of 2020 were broadly based, Pembroke’s Canadian equity mandates performed well on a relative basis too, outpacing both the S&P/TSX Composite and Completion Indices. From an industry group perspective, investments in the technology, consumer discretionary, industrial, and financial sectors were the largest contributors to the gains experienced during the quarter.

Two stocks made significant positive contributions to returns in the second quarter.

Two stocks made significant positive contributions to returns in the second quarter.

Shares in Kinaxis (“KXS”), a cloud-based provider of supply chain planning software, surged in the second quarter of 2020 as the company reported strong financial results. Moreover, management indicated that demand for its core offering, RapidResponse, is accelerating as organizations are relying on the company’s concurrent planning solutions to navigate disruptions caused by COVID-19. Drawing on its strong balance sheet, the company made two acquisitions in order to enhance their artificial intelligence forecasting abilities, increase supply chain resiliency, and further penetrate into new and existing verticals. With its market leadership, strong financial position, and management’s ability to strike a balance between growth and profitability, Kinaxis is positioned to remain a long-term structural winner in Canada.

Shares in BRP (“DOO”), a manufacturer, distributor, and marketer of recreational powersport and marine products worldwide, rebounded sharply in the second quarter. After shutting down its factories for two months due to COVID-19-related governmental restrictions, BRP is now struggling to keep up with strong retail demand for its line of side-by-side vehicles, ATVs and marine products. Confined at home, consumers are reallocating their vacation and leisure budgets to “COVID-compliant” alternatives such as powersports in a scenario analogous to that which occurred following 9/11. As a result, many of BRP’s products are out of stock at dealers. Responding to demand and replenishing dealer inventory levels may carry BRP’s sales well into 2021 and support earnings despite the economic recession and the discretionary aspect of their products.

Two stocks made significant negative contributions to returns in the second quarter.

Shares in Evertz Technologies (“ET”), a global provider of broadcast equipment and solutions that deliver content to televisions, on-demand services, streaming services, and mobile devices, declined in the second quarter as COVID-19 travel restrictions impaired the company’s ability to complete installations of its systems as originally scheduled. Furthermore, the cancellation of live sporting and entertainment events negatively impacted near-term demand for Evertz’ systems. While the company has a debt-free balance sheet, management chose to cut the dividend in order to preserve financial flexibility and free up capital for potential acquisition opportunities. In the longer-term, COVID-19 should spur increased demand for efficiently broadcast content; Evertz remains well positioned to capitalize on this trend.

Shares in Currency Exchange International (“CXI”), an operator of 45 retail foreign exchange locations and a provider of comprehensive foreign exchange and payment services to business customers, were weak in the second quarter. Uncertainty as to the timeline for the resumption of global tourist travel weighed on the outlook for the company’s retail foreign exchange operations, overshadowing progress in the company’s business-to-business segment. Still, the company remains well capitalized to weather COVID-19 related disruptions, particularly relative to smaller competitors.

Pembroke Dividend Fund Commentary

The Pembroke Dividend Growth Fund posted strong gains in the second quarter of 2020, rebounding from a difficult first quarter that was marred by COVID-19 driven disruptions and uncertainty. While visibility regarding the path to economic recovery remains limited, global actions taken by monetary and fiscal authorities have proven sufficiently decisive to persuade equity market investors to re-embrace risk.

On a relative performance basis, the fund outperformed both the S&P/TSX Composite Index and the S&P/TSX Dividend Aristocrats Index during the quarter. While the fund trailed the higher beta S&P/TSX Completion and Small Cap indices in the second quarter, it remains comfortably ahead of both those indices on a year-to-date basis.

Industry group performance reflected the broad-based nature of the second quarter rally, with only the fund’s communications holdings in negative territory for the period. Investments in the technology, consumer discretionary, industrial, and financial sectors were the largest contributors to gains during the quarter.

Two stocks made significant positive contributors to performance in the second quarter of 2020.

Shares of Collectors Universe (“CLCT”), a leading provider of third-party authentication and grading services for high-value collectibles such as coins and trading cards, rallied in the second quarter to new all-time highs. While the company experienced disruptions in March and April due to shelter-in-place orders in effect in California, the company was met with unprecedented demand upon resuming operations as COVID-19 isolation measures led to a resurgence in interest in hobbyist collecting. Additionally, an activist investor announced a significant position in the company in June and is encouraging the board of directors to take actions to enhance the company’s place in the transactional portion of the industry. This had the effect of further piquing interest in the Collectors Universe story.

Shares in Richards Packaging (“RPI.UN”), a distributor of plastic and glass containers to small and medium sized businesses and a distributor of healthcare packaging and dispensing systems to pharmacies, performed well in the second quarter. The company has been the beneficiary of a surge in demand for sanitizer and disinfectant products, as well as the pumps, sprays, and nozzles used to dispense them. We believe it is likely that demand will remain elevated compared to pre-pandemic levels as more stringent sanitization and disinfection protocols become the norm in a post-COVID-19 world. Moreover, the company bolstered its growth profile with the sizable acquisition of a complementary business in the healthcare distribution space.

Two stocks made significant negative contributors to performance in the second quarter of 2020.

Shares in Evertz Technologies (“ET”), a leading provider of content delivery systems servicing the broadcast television, on-demand television, streaming, and mobile markets, were weak in the second quarter. COVID-19 containment measures prevented the company from completing customer installations in a timely matter. Additionally, the company’s short-term outlook was negatively impacted by the cancellation of live sports, entertainment, and political events, which contribute to revenues on an episodic basis. While the board of directors scaled back the company’s dividend policy out of conservatism and to preserve capital for potential acquisition opportunities, we believe that longer-term prospects remain attractive for Evertz as COVID-19 should ultimately drive increased demand for efficient and cost-effective content delivery solutions.

Shares in Cogeco Inc. (“CGO”), a cable service provider with a network spanning Ontario, Québec, and the east coast of the United States, declined in the second quarter as a result of fallout from the COVID-19 pandemic. While the company’s cable assets are seeing reasonable stability in a difficult environment, the company owns twenty-two radio stations whose advertising revenues have shrunk as retail customers slash their marketing budgets amidst store closures. Despite near-term headwinds, Cogeco remains well-financed and its dividend payout ratio is conservative.

US Equity Strategies

US GROWTH EQUITY STRATEGY – Q2 PORTFOLIO COMMENTARY

Pembroke’s US portfolios rebounded after a difficult first quarter. Additionally, the firm’s stock selection and allocation to well-positioned industry groups helped drive outperformance versus the Russell 2000 Index. Holdings in the information technology, industrial, and consumer discretionary sectors drove significant gains in the past three months. During the first half of the year, the investment team reduced holdings in companies whose business models were negatively impacted by COVID-19, added to holdings whose business models were unaffected in the medium to long-term, and increased exposure to companies positioned to benefit from the changed circumstances. The outcome of these decisions is a portfolio that is better-financed, growing faster, and more competitively positioned than before the COVID-19 crisis erupted. Further, Pembroke initiated new positions in several companies, finding entry points that offered a favourable risk/reward profile. Overall, it was satisfying to see the team’s focus on quality, growth, and balance sheet strength rewarded coming out of the first quarter.

Shares in Installed Building Products (“IBP”), returned close to 70% in the second quarter, due to a combination of both market-level and segment-level macro factors. On the market side, the belief that COVID-19 would not permanently impair the US and global economies contributed to the stock’s sharp recovery following an equally sharp decline in Q1. On the segment level, signs of strong pent-up demand for housing and a quick resumption in home construction activity led investors to regain confidence in stocks like IBP that provide materials and services to US homebuilders. While IBP’s Achilles heel remains its cyclicality, it has generated consistently high returns on capital, has a compelling growth strategy, and is led by a shareholder-aligned and effective management team. As such, it remains a core position.

The recent share price performance of Kornit Digital (“KRNT”), which sells machines that allow clothing manufacturers to efficiently execute limited product runs, is an example of investor short-termism manifesting itself in violent near-term trading swings. In March, the shares dropped 50% from their peak as investors fretted that not only would new machine sales abate, but factories using existing machines would shut and ink sales would fall dramatically. Admittedly, the environment during the COVID-19 pandemic is not conducive to new sales of digital printing machines, but the long-term opportunity remains compelling and Kornit is capitalized to see its way through the current slowdown. The price decline presented an opportunity, and Pembroke increased its weight in the investment during this period. Following the company’s first quarter report and management commentary that not only disabused investors of their worst fears but gave them reason for optimism, the share price retraced all of its losses.

During the quarter, Pembroke sold its position in Vocera Communications (“VCRA”), which provides communications equipment to hospitals. The need to improve patient care and provide better working environments and communication systems for nurses and doctors is real. Pembroke’s investment team, nevertheless, decided that Vocera’s offerings would not find themselves at the top of many hospitals’ capital budgets in an environment where they are facing major headwinds from reduced elective procedures which are critical to hospital profits. Further, Vocera had faced execution challenges in recent years as sales cycles elongated and the company transitioned to a next-generation version of its core product. The holding was sold while Pembroke maintained and invested in other healthcare companies.

Despite the company reporting solid Q1 results, Healthstream’s (“HSTM”) stock languished in the second quarter of 2020 as the business outlook weakened on the impact of COVID-19. Several of its hospital clients have been negatively impacted by the postponement of elective procedures. As a result, they have laid off or furloughed workers and delayed systems implementations, including those tied to workforce training offered by Healthstream. The company continues to gain share and more normal patient flows are returning as states lift restrictions on elective procedures. The environment, however, remains rocky and the second wave of COVID-19 patients taking up hospital beds is not helping. The company has a compelling business model and large market opportunity but is held at a small weight in Pembroke’s US portfolios as it has not delivered consistent growth.

CONCENTRATED GROWTH EQUITY STRATEGY – Q2 PORTFOLIO COMMENTARY

The Pembroke Concentrated Fund gained by 36.7% during the quarter, outperforming its benchmark the Russell 2000 Index which gained by 20.5% during the quarter. Given the magnitude of the benchmark’s recovery during the quarter, the concentrated fund’s excess return of 16.2%, with only 17 holdings, is a testament to the strategy’s strict discipline and focus on high-quality growth companies. Since its inception on January 31, 2018, the fund has posted a 16.7% annualized return compared to the Russell 2000 Benchmark’s annualized return of 2.1%, an excess annualized return of 14.6%.

The main source of excess return during the quarter was the fund’s security selection in the information technology (IT) sector where eight of the fund’s nine IT holdings advanced and seven of the nine advanced more than the benchmark’s IT sector average. The fund’s industrial sector holdings also added value. The fund’s IT and industrial sector holdings account for 65% of the fund’s weight. The fund’s zero allocation to financials and materials also contributed to positive relative performance. The fund’s health care and consumer discretionary holdings all gained during the quarter but did not keep pace with the benchmark’s sector averages. Approximately 89% of the fund was invested in the US at quarter-end and 11% in Canada.

Two stocks made notable positive contributions to returns during the quarter:

Shares in Kinaxis (“KXS CN”), a cloud-based provider of supply chain planning software, gained in the second quarter of 2020 as the company reported strong financial results. Moreover, management indicated that demand for its core offering, RapidResponse, is accelerating as organizations are relying on the company’s concurrent planning solutions to navigate disruptions caused by COVID-19. Drawing on its strong balance sheet, the company made two acquisitions in order to enhance their artificial intelligence forecasting abilities, increase supply chain resiliency, and further penetrate into new and existing verticals. With its market leadership, strong financial position, and management’s ability to strike a balance between growth and profitability, Kinaxis is positioned to remain a long-term structural winner in Canada.

Shares in Installed Building Products (“IBP US”), returned close to 70% in the second quarter, due to a combination of both market-level and segment-level macro factors. On the market side, the belief that COVID-19 would not permanently impair the US and global economies contributed to the stock’s sharp recovery following an equally sharp decline in Q1. On the segment level, signs of strong pent-up demand for housing and a quick resumption in home construction activity led investors to regain confidence in stocks like IBP that provide materials and services to US homebuilders. While IBP’s Achilles heel remains its cyclicality, it has generated consistently high returns on capital, has a compelling growth strategy, and is led by a shareholder-aligned and effective management team. As such, it remains a core position.

Two stocks made notable negative contributions to returns during the quarter:

The shares of Euronet Worldwide (“EEFT US”) declined during the second quarter. The company provides secure electronic financial transactions (EFT) solutions including a global payment network for prepaid mobile top-up, a global money transfer company, and an independent international ATM network. With clients in some 170 countries, the company announced that global population movement restriction measures had resulted in decreases in business transactions in some areas (international transactions in the EFT business) and increases in other areas (the money transfer segment). The impact on the electronics payments business has so far been mixed with some negative impacts in areas where population restriction measures are in place and some positive impacts from increased use of mobile devices, streaming, and gaming. The company prudently announced in March that first quarter results could not be reasonably estimated, and it withdrew its previously issued first quarter guidance.

The shares of Globus Medical (“GMED US”) gained during the second quarter but did not keep up with the benchmark and therefore made a negative contribution to relative performance. The company, a leading musculoskeletal implant manufacturer with expertise in computer-assisted robotic spine surgery solutions, withdrew previously announced full-year guidance in April due to uncertainties resulting from the COVID-19 pandemic. Despite industry concerns about delays for spinal procedures and hospital budget cuts, the company announced first quarter sales increases of more than 4% along with the launch of three new spine products. The company also highlighted its conservative financial situation and ability to maintain its long-term growth initiatives.

International Equity Strategies

Q2 and Six-month Review

The Pembroke International Growth Fund outpaced the MSCI ACWI ex-US Small Cap Index during the quarter and year to date periods ended June 30. The fund’s emphasis on high-quality growth companies with strong financial positions bolstered relative performance amid the COVID-19 pandemic-driven market correction in March, while contributing to subsequent outperformance as financial markets strongly recovered in the April-June period.

Stock selection within the industrials and information technology sectors were key drivers of outperformance during the second quarter and six-month period ended June 30. The overweighting to information technology stocks and underweightings to energy and real estate stocks also contributed positively to relative performance.

Within industrials, Japanese holdings Nihon M&A Center and Monotaro were top contributors during both the quarter and six-month periods. Nihon M&A Center is a high-quality Japanese growth company that provides advisory services to small and medium-size enterprises (SMEs) facing succession-oriented challenges. It is led by an entrepreneurial management team that has built an attractive network of national relationships aimed at identifying buyers and sellers and sourcing transactions. Maintenance, repair and operations company Monotaro offers over 10m products across seven industrial categories using a single transparent price for each product and overnight delivery. The company uses its extensive customer database to predict client order trends, apply targeted promotions, and manage inventory.

Within the information technology sector, Chinese semiconductor company Silergy was the top performer for the quarter and six-month periods. Silergy is a fabless analog semiconductor company with expertise in power management integrated circuits. Its competitive advantage is its ability to design products with superior performance at a low cost.

Partially offsetting these positive contributors were negative stock selection in healthcare and the underweighting to materials stocks. Within the healthcare sector, Germany-based Carl Zeiss Meditec was the largest detractor during the quarter and six-month periods. Carl Zeiss is one of the leading suppliers of surgical tools and equipment for the diagnosis and treatment of ophthalmic conditions. The company has a history of innovation that has a provided them a strong platform from which to expand into lucrative adjacencies such as intraocular lens (IOLs), the largest market within surgical ophthalmology. The share price was negatively impacted by COVID-19 lockdowns and weak patient volumes.

Fixed Income & Balanced Strategies

Canadian Bond Strategies – Q1 Portfolio Commentary

Markets came roaring back in spectacular fashion from their pandemic-induced first quarter selloff. This performance was helped by massive government assistance and central bank actions. The US Federal Reserve has implemented a number of “funding, credit, liquidity, and loan facilities.” These include the direct purchase of corporate bonds and related ETFs in both the primary and secondary markets. The Bank of Canada has implemented similar programs, on a smaller scale.

Overall, credit spreads narrowed, especially in those sectors least affected by the pandemic. As a result, corporate bonds outperformed Canada bonds by a wide margin with a return of 8.1% versus 2.3%. This spread tightening had the greatest price impact on long-term bonds, and longer duration Provincials were also strong performers. The AA and higher corporate sector is dominated by short-term financials and its 4.1% return underperformed the broader corporate market. Spreads narrowed significantly on A-rated bonds and even more on BBB bonds which returned 8.4% and 9.7% respectively.

Pembroke Canadian Bond Fund Commentary

The Canadian Bond Fund returned 5.9% in the quarter which was in line with the FTSE Canada Universe Bond Index return of 5.9%. The fund benefited from spread narrowing on corporate bonds and the impact of the significant stimulus measures. The fund purchased high-quality issues such as TD and CIBC Bank deposit notes, NAV Canada, and Toyota Credit Canada that were available at very attractive yields. The fund finished the quarter with a yield to maturity of 1.7% and a duration of 6.6 years. While market yields remain at very low levels, the fund’s yield compares favourably to the index yield of 1.3%.The fund’s duration is also notably shorter than the index’s duration of 8.5 years.

Pembroke Corporate Bond Fund Commentary

The Corporate Bond Fund returned 11.6% in the quarter compared with the corporate index return of 8.1%. The fund benefited from the impact of the significant stimulus measures and the return of liquidity to the market. Canso was active buying corporate bonds early in the quarter in the primary and secondary markets at attractive levels. This led to substantial outperformance as spreads narrowed and prices recovered, particularly in the oil and gas and car rental industries. Canso continues to identify stressed companies that have sufficient short-term liquidity, good medium to long-term prospects, and the prospect of solid risk-adjusted returns. With a yield to maturity of 6.6% and a duration of 4.1 years, the fund is well positioned going forward.

Pembroke Canadian Balanced Fund Commentary

Pembroke’s Canadian balanced portfolio, the Pembroke Growth and Income Fund, reported strong returns in the second quarter of 2020. Performance was driven by gains in the equity portion of the portfolio, represented by the holdings of the Pembroke Dividend Growth Fund, as well as a recovery in the fixed income portion of the fund, represented by the Pembroke Canadian Bond Fund.

Equity returns of the fund were driven by a restoration of market confidence following decisive fiscal and monetary measures enacted to counter the fallout from COVID-19. Similarly, fixed income investments of the fund experienced price increases as credit spreads narrowed, reflecting greater investor confidence in the ability of corporate borrowers to service their debt obligations.

Income in the balanced fund is generated from a combination of dividends and interest. The equity portion of the fund has a current annualized gross yield of 2.3%, while the fixed income segment of the fund is primarily invested in securities rated “A+” that, on average, have a collective yield to maturity of 1.7% and an adjusted portfolio duration of 6.6 years. The asset mix of Pembroke’s Canadian balanced mandates did not change materially through the year, with approximately 30% of the portfolio invested in fixed income securities at June 30, 2020.

Pembroke Global Balanced Fund Commentary

The Pembroke Global Balanced Fund is a fund of funds that invests primarily in Pembroke-managed equity and bond funds, externally managed active funds, and externally managed passive funds and exchange-traded-funds (ETFs). During the quarter, the fund gained approximately 17.2% compared to its benchmark (30% Canadian Universal Bond Index, 45% MSCI All-Country World Index, and 25% S&P TSX Composite Index), which gained 12.5%.

During the second quarter the fund maintained its diversification by asset class, by region, by factor (small cap and large cap), and by fund type (active and passive). At the end of the quarter the fund had a 69% allocation to global equities and a 31% allocation to Canadian corporate and sovereign bonds and cash.

The fund’s active equity allocations benefitted from the managers’ focus on high-quality growth companies in markets across the world. The funds also benefitted from a very low exposure to the energy sector and a meaningful exposure to the information technology sector.

The bond allocation is largely to the Pembroke Corporate Bond Fund which outperformed its benchmark during the quarter. At the end of the quarter, the corporate bond fund had a yield to maturity of 6.6% and a duration of 4.1 years compared with its benchmark the FTSE Canada All Corporate Bond Index which had a yield to maturity of 2.1% and a duration of 7.0 years. During the quarter, the corporate bond fund returned 11.6% compared with the benchmark’s 8.1%. The corporate bond fund’s low duration should position it well if rates rise from their historically low levels.

Virtual Lunch Series

Managing Portfolios During Uncertain Times

As we continue to share our insights while maintaining appropriate social distance, we invite you to join us for a virtual lunches/brunches:

- Thursday, July 23rd at 10:30AM (Eastern Daylight Time), focus on Pembroke’s Perspective on Investing in Growth and Disruption with Matthew Beckerleg and Andrew Garschagen;

Wednesday, August 19th at 11:00AM (Eastern Daylight Time), focus on ESG with David Whittall. - An invitation with details will be sent out by email, if you do not receive a copy and wish to join our virtual lunch, please contact your Pembroke Representative for details.

If you missed any of our Pembroke Virtual Lunch Series, you can replay our virtual lunches here.

Just the Facts

Top Five Canadian & US Holdings

Top Five US Holdings

Top Five canadian Holdings

Source: Bloomberg consensus estimates, some of which are under review.

In the Community

Pembroke has been the lead sponsor of the Montreal Highland Games for several years. Like virtually all other events, the Games have been cancelled this summer due to the pandemic. In their place, Pembroke is pleased to be the title sponsor of an on-line piping competition organized by the Montreal Highland Games Society that will be taking place this August. In addition, Ian Aitken and his son have been working with the St. Andrew’s Society on the Pandemic Piper Project which has solo pipers play in iconic locations around the city of Montreal. “During what is a very difficult time for many people, this project is a positive activity that we hope will bring a smile to the faces of many” said Ian Aitken. Videos of the short performances, which are released weekly, can be viewed on the website of the St. Andrew’s Society.

Disclaimer

This report is for the purpose of providing some insight into Pembroke and the Pembroke funds. Past performance is not indicative of future returns. Any securities listed herein, are for informational purposes only and are not intended and should not be construed as investment advice nor is it a recommendation to buy or sell any particular security. Factual information has been taken from sources we believe to be reliable, but its accuracy, completeness or interpretation cannot be guaranteed. Pembroke seeks to ensure that the content of this document is correct and up to date but does not guarantee that the content is accurate and complete and does not assume any responsibility for this. Pembroke is not responsible for decisions or actions taken or made on the basis of information contained in this document.

Publication Date: July 31, 2020